- This topic has 2,797 replies, 193 voices, and was last updated 11 years, 7 months ago by

D C.

D C.

-

CreatorTopic

-

May 14, 2014 at 3:33 pm #185549jeffKeymaster

Free Study Planner, Notes, Audio, Flashcards: https://www.another71.com/cpa-exam-study-plan/

Free CPA Exam Survival Guide: https://www.another71.com/cpa-exam-survival-guide/

-

AuthorReplies

-

August 14, 2014 at 2:50 pm #599936jstayParticipant

ughhhhh

August 14, 2014 at 3:16 pm #599937AnonymousInactiveI submitted the inquiry and got this answer from Gleim:

“Please note that financial depreciation in excess of tax depreciation in future years will result in greater taxable income and therefore more taxes owed. When this occurs due to accelerated tax depreciation (as in Year 4), then the later difference (Years 6, 7, and 8) will be classified as a deferred tax liability.”

Does this make sense? I am so confused, I thought I knew deferred taxes.

Doesn't financial depreciation in excess of tax depreciation = DTA?

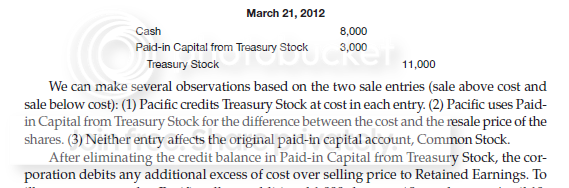

August 14, 2014 at 4:09 pm #599938D CMemberNinja is correct. APIC C/S is reduced first. then remaining balance from RE.

You have no blanche in APIC T/S to begin with so you have nothing to reduce. You only have APIC-C/S, then RE is a last resort.

You cannot carry a credit balance in APIC T/S.

B - 80

A - 71, 67, 77

R - 71, 77

F - 72, 77

DONE!!

Becker Self-study all the way! Did use Ninja Notes & Audio for FAR.August 14, 2014 at 4:18 pm #599939jstayParticipantso say you had a 20,000 balance in APIC – T/S. you would debit 20,000 and then debit apic-C/S for 100,000 and not RE

August 14, 2014 at 4:22 pm #599940D CMemberyup

B - 80

A - 71, 67, 77

R - 71, 77

F - 72, 77

DONE!!

Becker Self-study all the way! Did use Ninja Notes & Audio for FAR.August 14, 2014 at 4:28 pm #599941AnonymousInactiveI looked it up in my Nikolai/Bazley/Jones, their example shows that only apic-ts is reduced. Not sure what is the source of all these rules

August 14, 2014 at 5:04 pm #599942Iggy1985MemberQuick and probably dumb question; why does a bond payable qualify as a hybrid instrument that requires bifurcation under derivatives and hedging, if debt and equity securities don't qualify as derivatives?

Which of the following qualifies as a hybrid instrument that would require bifurcation under ASC Topic 815, Derivatives and Hedging?

I. A bond payable with an interest rate based on the S & P 500 Index.

II. An equity instrument with a call option, allowing the issuing company to buy back the stock.

Both I and II.

.This answer is correct. Both items qualify as hybrid instruments that would require bifurcation under ASC Topic 815. The process of bifurcation separates an embedded derivative instrument from the basic or “host” contract.

FAR - 89 (8/19/14) Wiley TB, Wiley Book, Books from School, Ninja Audio/Notes

AUD - 92 (10/14/14) Wiley TB, Wiley Book, Ninja Audio

BEC - 82 (5/8/15) Mostly Ninja MCQ, sprinkles of Becker lectures and Ninja Audio

REG - (8/14/15)August 14, 2014 at 5:22 pm #599943D CMemberThere is no balance in the APIC T/S account to reduce from.

Also correction on my last post: APIC T/S cannot carry a debit balance. APIC T/S has a natural credit balance (same as APIC T/S)

In my opinion I agree with everyone that they should not reduce APIC-C/S and go straight to RE. It seems like a mismatch/commingling of accounts that don't belong together.

B - 80

A - 71, 67, 77

R - 71, 77

F - 72, 77

DONE!!

Becker Self-study all the way! Did use Ninja Notes & Audio for FAR.August 14, 2014 at 5:36 pm #599944Iggy1985MemberI also had a similar question in Wiley regarding APIC T/S vs C/S, and the answer explanation said that APIC from previous transactions can be used or alternatively entire debit to R/E.. wish I had an easy way to bring it up again.. edit.. found it.. this is on retirement but same concept right?

The stockholders’ equity section of Peter Corporation’s balance sheet at December 31, year 1, was as follows:

Common stock ($10 par value, authorized 1,000,000 shares, issued and outstanding 900,000 shares) $ 9,000,000

Additional paid-in capital (APIC) 2,700,000

Retained earnings (RE) 1,300,000

Total stockholders’ equity $13,000,000

On January 2, year 2, Peter purchased and retired 100,000 shares of its stock for $1,800,000. Immediately after retirement of these 100,000 shares, the balances in the additional paid-in capital and retained earnings accounts should be

$2,400,000

$ 800,000

The solutions approach is to make the journal entry to record the retirement.

Common stock 1,000,000

Additional paid-in capital 300,000

Retained earnings 500,000

Cash 1,800,000

Common stock is debited for $1,000,000 par value ($10 per share × 100,000 shares). APIC can be debited for either the APIC from previous retirements or the pro rata portion of APIC for the current issue; the second alternative applies to this question. One-ninth of the shares of common stock are retired, so one-ninth of APIC can be debited for $300,000. An additional debit to RE is required for $500,000 ($1,800,000 – $1,000,000 – $300,000). Therefore, the balances of APIC and RE after retirement of 100,000 shares are $2,400,000 ($2,700,000 – $300,000) and $800,000 ($1,300,000 – $500,000) respectively.

Formal retirement or constructive retirement (purchase with no intent of reissue) of stock is handled very similarly to treasury stock. When formally retired

dr Common stock xx

dr Paid-in capital in excess of par* xx

dr Retained earnings* xx

cr Treasury stock* xx

* Assuming a loss on the retirement of treasury stock

1. “Paid-in capital from treasury stock transactions” may be debited to the extent it exists

2. A pro rata portion of all paid-in capital existing for that issue (e.g., if 2% of an issue is retired, up to 2% of all existing paid-in capital for that issue may be debited)

Alternatively, the entire or any portion of the loss may be debited to retained earnings. Any gains are credited to a “paid-in capital from retirement” account.

FAR - 89 (8/19/14) Wiley TB, Wiley Book, Books from School, Ninja Audio/Notes

AUD - 92 (10/14/14) Wiley TB, Wiley Book, Ninja Audio

BEC - 82 (5/8/15) Mostly Ninja MCQ, sprinkles of Becker lectures and Ninja Audio

REG - (8/14/15)August 14, 2014 at 5:40 pm #599945D CMember@iggy

I don't really know much about your bond questions.

Only time Bond is “bifurcated” is when its a convertible bond under IFRS – a equity and liability must be recognized at time of issue. unlink GAAP where convertible bonds don't get any separate recognition, you just end up paying a premium for the conversion feature..

not sure if that has anything to do with it but its the only that comes to my mind at the moment.

B - 80

A - 71, 67, 77

R - 71, 77

F - 72, 77

DONE!!

Becker Self-study all the way! Did use Ninja Notes & Audio for FAR.August 14, 2014 at 6:03 pm #599946Iggy1985MemberMy intermediate textbook (kieso) only states that you debit apic-c/s (the portion applicable to the shares) when retiring, not reissuing, treasury stock, so I'm not sure that Gleim is correct

https://img.photobucket.com/albums/v301/Vixia/sdgsdgsdg_zpsc7bf8e9e.png

FAR - 89 (8/19/14) Wiley TB, Wiley Book, Books from School, Ninja Audio/Notes

AUD - 92 (10/14/14) Wiley TB, Wiley Book, Ninja Audio

BEC - 82 (5/8/15) Mostly Ninja MCQ, sprinkles of Becker lectures and Ninja Audio

REG - (8/14/15)August 14, 2014 at 7:48 pm #599947jstayParticipantis it possible to move up a test date?

August 14, 2014 at 8:34 pm #599948Iggy1985Memberyes but you'll be charged (~$35?) if it's within 30 days of what you have scheduled

FAR - 89 (8/19/14) Wiley TB, Wiley Book, Books from School, Ninja Audio/Notes

AUD - 92 (10/14/14) Wiley TB, Wiley Book, Ninja Audio

BEC - 82 (5/8/15) Mostly Ninja MCQ, sprinkles of Becker lectures and Ninja Audio

REG - (8/14/15)August 14, 2014 at 9:12 pm #599949nosleep135Member@jstay, I am also considering moving my date up to October…if I remember correctly, you are also scheduled for Aug 31 (if only I could remember the material this easily!)

August 14, 2014 at 9:23 pm #599950jstayParticipanti meant move it up as in closer, i am scheduled for 8/31 but I'm looking maybe for 8/24

-

AuthorReplies

{kind=link}

- The topic ‘[Q3] FAR Study Group 2014 - Page 163’ is closed to new replies.