- This topic has 66 replies, 12 voices, and was last updated 11 years, 10 months ago by

.

.

-

Topic

-

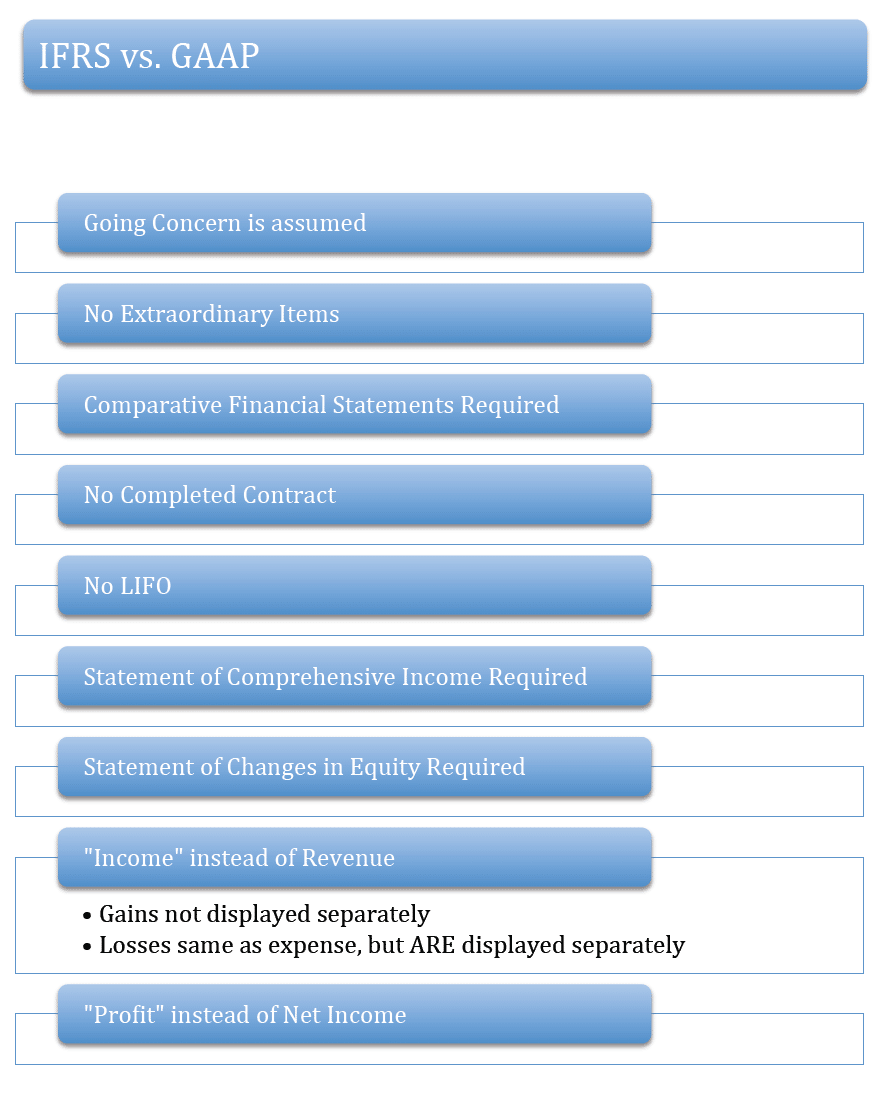

Let’s a full list going here as a quick reference guide for everyone studying. So far from the FAR discussion forum we have the following:

#1: Extraordinary items – GAAP/Yes and IFRS/Not allowed

#2: IFRS does NOT allow the completed contract method.

#3: Inventory: Differences between GAAP and IFRS

1. GAAP can choose between LIFO and FIFO…………………………….. IFRS LIFO is prohibited

2. GAAP inventory is carried at lower of cost or replacement cost………IFRS it is lower of cost or NRV

3. GAAP inventory write-downs cannot be reversed. ….IFRS if impairments no longer exist, the inventory can be written up back up.

BEC: 65 - 79* - 84 DONE

AUD: 65 - 76 DONE

REG: 63 - 77 DONE

FAR: 65 - 63 - 67 - 69 - 73 - 71 - 83 DONEBecker Notes & Flashcards, Wiley Test Bank, Ninja MCQ

{kind=link}

- The topic ‘IFRS vs. GAAP: - Page 2’ is closed to new replies.